The problem with financial aid award letters

Let’s say you’re a financial aid officer preparing a letter laying out your school’s aid offer to an accepted high school senior. Would you list a student loan without using the word “loan”? Would you tell the student that the “net cost” to attend your school is $0—but only when you include work-study money that she has to earn and loans that she’ll have to repay?

Probably not, but many financial aid officers are doing all these things and more.

Spurred on by misleading and confusing language in award letters, uAspire and the New America Foundation conducted a recent study called “Decoding the Cost of College: The Case for Transparent Financial Aid Award Letters.” It analyzed more than 11,000 letters and found that:

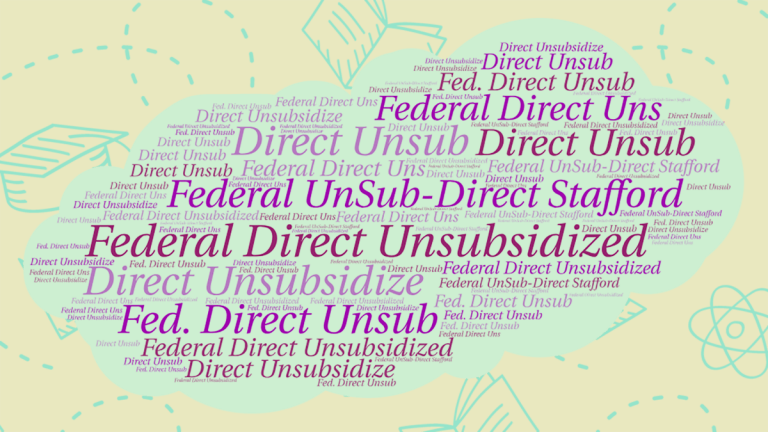

- Colleges referred to an unsubsidized federal student loan with 136 different terms—often without even using the word “loan.” (“Fed Direct Unsub L,” anyone?)

- 70% lumped aid together without differentiating between loans (borrowed money), scholarships and grants (free money), and work-study (earned money).

- 50% of the letters failed to specify next steps, e.g., how to accept or decline loans.

- 15% mixed in a Parent PLUS loan (expensive federal parent loans that families should consider only as a last resort) with student aid.

Recently, uAspire, an organization that helps underserved students find affordable ways to attend college, hosted a presentation in New York City to go deeper into the problems with financial aid letters, and to offer views from an expert panel. (Full disclosure: I was honored to get uAspire’s seal of approval for my recent multimedia project, We Need to Talk: College.)

One panelist, Zayne Abdessalam, director of policy and research at the Office of Financial Empowerment in New York City’s Department of Consumer Affairs, bemoaned the low standards for these all-important letters. After all, financial aid is often a make-or-break issue for students looking to avoid taking on major debt.

“College shoppers are missing critical information,” Abdessalam said. “We recently put in place rules for used car salesmen that are more strict than the rules for these financial aid letters.”

There are guidelines for how these letters should look. The government’s Financial Aid Shopping Sheet, introduced by the Obama Administration in 2013, is a model for clear, standardized letters, but while its use is required when colleges contact military service members and veterans (who are frequent targets of shady lenders), it’s optional for everyone else. Even for schools acting in good faith, the shopping sheet can be problematic. “It lacked the ability for customization,” said Christen O’Connor, associate director of financial aid at Dartmouth College, which sends its accepted students one of the more transparent letters out there. As the National Association of Student Financial Aid Administrators (NASFAA) notes, “financial aid offices know their student populations best, and need flexibility to design award notifications that meet those students’ needs.”

For schools acting in bad faith, an opaque and confusing financial aid letter is in their best interest. According to uAspire’s report, it serves as “an enrollment management tool to entice students to come to the school by making it appear as if all the costs are covered.” O’Connor recounted getting calls from families asking Dartmouth to match another school’s offer, only to find, upon closer reading of the competing offer, that the other school was offering less money. Families just couldn’t decipher the facts.

Oftentimes, neither can high school college counselors.

“It’s terrible, it’s agonizing,” said Flosha “Flow” Tejada, director of college completion at Uncommon Collegiate Charter High School in Brooklyn. “None of my students fully understood the letters.”

Searching for a method to prepare families, Brendan Williams, director of knowledge at uAspire, analyzed tens of thousands of award letters. His solution: Show them old award letters. “Looking at comparable students’ letters can be helpful,” Williams said. As it turns out, viewing letters received by kids with similar financial circumstances helps settle frayed nerves and gives families an inkling of what financial aid details to anticipate for their own kid, Williams said.

Dartmouth’s O’Connor had her own advice. “Utilize financial aid officers as a resource. Have them explain the letter,” she said. “We didn’t get into this profession to get rich. We did it because we care about college access and affordability.”

The bottom line: 17-year-olds shouldn’t have to decipher a confusing financial aid offer. And while there are some resources out there (the Consumer Financial Protection Bureau’s Financial Aid Comparison Tool is one), until families know they are comparing apples to apples in terms of offers, this step will continue to add more stress to an already stressful college process.

So what’s the answer? The uAspire/New America report says the federal government should “set and require award letter standards via federal mandate akin to other consumer standardization such as the HUD-1 settlement sheet and credit card statements.”

Whether it’s a one-size-fits-all design, as the report recommends, or just a standardization of terms and elements, as NAFSAA desires, any new requirements should, at a minimum, allow students and families to make informed choices without undue stress or a secret decoder ring.